Professional Liability Insurance is one of the most misunderstood - and most important - policies a Dallas professional can carry. The figures quoted online are often generic, the coverage details glossed over, and too many businesses end up either underinsured or paying for a policy that wouldn't hold up when it matters most.

This guide is designed to give Dallas professionals a clear, honest picture of what PLI actually costs in 2026, what drives those figures, and how to make sure your coverage is genuinely built around your exposure - not just a price point.

By reading this guide, you'll understand:

-

What Professional Liability Insurance typically costs in Dallas, with figures broken down by profession.

-

The key risk factors that influence your premium - and how underwriters assess them.

-

The important distinction between professional liability and general liability coverage, and why most businesses need both.

-

How to structure your coverage so it actually responds when a claim arises.

-

Why Texas's legal environment affects how your risk should be placed - and with whom.

Prefer to speak to someone directly? A dedicated Risk Advisor will assess your exposure and place your coverage where it belongs. Call 972.991.9100

What Is Professional Liability Insurance and Why Do Dallas Professionals Need It?

Professional Liability Insurance (PLI), also known as Errors and Omissions (E&O) insurance, is designed to protect professionals from claims of negligence, mistakes, or omissions in the services they provide. Unlike General Liability Insurance, which covers physical injury and property damage, PLI covers legal defense costs, settlements, and judgments when clients claim financial loss due to professional errors.

For professionals in Dallas, this type of coverage is critical. Consider a real estate agent who faces a lawsuit for failing to disclose a defect in a property. Without professional liability insurance, the agent could be liable for significant legal fees and settlement costs.

Whether you're a lawyer, accountant, consultant, or healthcare provider, PLI provides essential protection against costly lawsuits, allowing you to focus on your business with peace of mind.

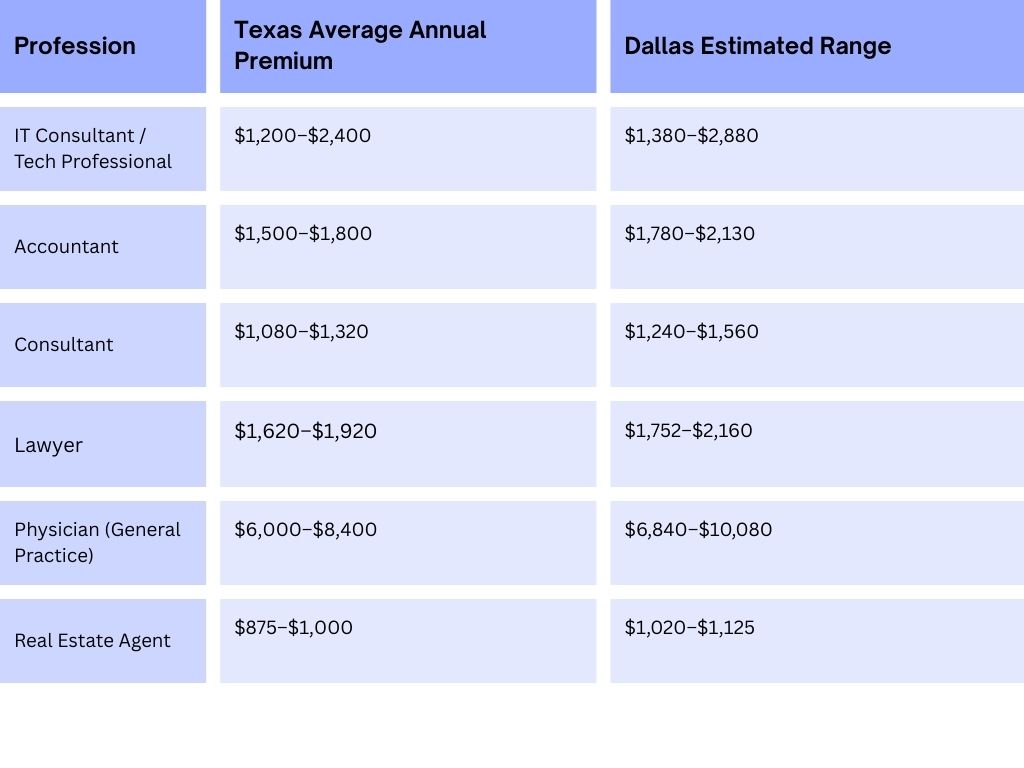

How Much Does Professional Liability Insurance Cost in Dallas, TX in 2026?

Premium figures give you a useful starting point, but they rarely tell the whole story. The cost of Professional Liability Insurance is ultimately a reflection of your risk profile - your profession, the nature of your client relationships, your claims history, and the limits and structure of the policy itself.

For context, small businesses in Texas pay an average of $73–$78 per month for PLI. Dallas professionals typically pay somewhat more, given the city's higher litigation volume and the concentration of complex commercial activity. But the more important question is not what the average is - it's whether your coverage is structured to respond correctly if a claim is made against you.

The figures below offer a general indication of what professionals in Dallas pay annually. Your Thumann Risk Advisor will assess your specific exposure and place your risk accordingly.

Note: Physician premiums vary significantly based on specialty. A general practitioner will typically sit at the lower end of this range, while specialists such as surgeons or anaesthesiologists may reach the upper end or beyond.

What Factors Influence Professional Liability Rates in Dallas?

Several factors affect the cost of Professional Liability Insurance. These include your profession, the risk level associated with your work, the limits of your policy, and your claims history.

Profession and Risk Level: High-risk professions such as healthcare and law typically face higher premiums because they are more likely to be sued. IT consultants and technology professionals are an increasingly significant category in Dallas's growing tech sector - and their exposure to data-related claims and software errors makes PLI equally important for them.

Policy Limits and Deductibles: The amount of coverage you need and the deductible you choose will impact your rates. Higher limits and lower deductibles usually mean higher premiums.

Claims History: Businesses with no claims history are often rewarded with lower premiums, while a history of claims can drive rates up.

Contractual Requirements: Many clients and employers now require proof of PLI before engaging a professional's services - particularly in healthcare, legal, and technology fields. Even where it isn't state-mandated, you may find it's effectively required to win contracts and bids.

Dallas-Specific Factors: Dallas's urban environment introduces additional risks, including a higher volume of litigation and a concentration of complex commercial activity. Texas tort reform has helped stabilise the broader insurance market, but the right carrier and policy structure for your profession still matters enormously - and that's where a Risk Advisor earns their keep.

How to Structure Your PLI Coverage Wisely

Getting PLI right isn't just about the premium — it's about making sure the policy is built around your actual exposure. Here are the key decisions that affect both the quality and cost of your coverage:

-

Work with an Independent Broker: Because Thumann Agency isn't tied to any single insurer, we place your risk with the carrier best suited to your profession and exposure — not whoever's offering the lowest headline rate. That distinction matters when a claim arises.

-

Consider a Business Owners Policy (BOP): For many professionals, combining PLI with general liability and property coverage under a single policy is not just more efficient — it's better coverage. Your Risk Advisor can assess whether a BOP is appropriate for your situation.

-

Set Your Deductible Thoughtfully: A higher deductible reduces your premium, but it should reflect what you can genuinely absorb. We'll help you find the right balance for your business size and cash flow.

-

Protect Your Claims Record: A clean claims history is one of the strongest signals to underwriters. Where possible, minor disputes are often better resolved directly — your Risk Advisor can help you think through when to claim and when not to.

Why Dallas Professionals Trust Thumann Agency

For nearly three decades, Thumann Agency has helped established Dallas businesses protect what they've worked hard to build. As independent brokers, we're not tied to any single insurer - we work across 80+ carriers to place your risk where it genuinely belongs, with coverage designed to hold up when it matters most.

Every client at Thumann Agency is assigned a dedicated Risk Advisor - not a salesperson, not a call centre. Someone who takes time to understand your business, your professional exposure, and the specific risks of your field, then builds coverage around that picture.

-

Independent Broker Access Across 80+ Carriers: We place your risk with the insurer best suited to your profession and exposure - not the one with the loudest marketing. That independence is what allows us to build coverage that actually fits.

-

30 Years of Dallas-Based Risk Expertise: Our advisors have spent decades working with Dallas professionals across law, medicine, finance, real estate, and technology. That depth of experience informs every placement we make.

-

Dedicated Risk Advisors, Not a Sales Team: You'll work with one person who understands your business and stays with you for the long term - reviewing your coverage as your practice grows and your exposure changes.

-

Same-Day COI Delivery: When a contract or bid requires proof of coverage quickly, we're ready. Our same-day Certificate of Insurance delivery means you're never held up waiting on paperwork.

-

Claims Advocacy When You Need It Most: If a claim arises, we don't hand you a phone number. We work alongside you through the process, making sure your insurer responds as the policy intends.

-

Sound Advice Over the Long Term: Thumann Agency has been a trusted partner across Texas for clients who value a broker that stays with them - not one that disappears after the policy is bound.

FAQs About Professional Liability Insurance in Dallas

What does Professional Liability Insurance cover?

Professional Liability Insurance covers legal defense costs, settlements, and judgments from claims of negligence or mistakes in the services you provide. It's essential for protecting professionals from lawsuits related to advice or services.

How much does Professional Liability Insurance cost in Dallas?

The Texas state average is $73 - $78 per month for small businesses. Dallas professionals may pay somewhat more depending on their profession, risk profile, and claims history. High-risk professions like law and healthcare will sit toward the higher end of the scale.

What factors influence my Professional Liability Insurance premium?

Your premium depends on your profession, claims history, coverage limits, and deductible. High-risk professions typically have higher premiums, and a clean claims history can lower your rate.

Do I need Professional Liability Insurance if I already have General Liability Insurance?

Yes. General Liability Insurance covers physical injury and property damage, while Professional Liability Insurance protects against claims related to mistakes or negligence in your services. Both serve different purposes and many businesses need both.

Are there professions that are contractually required to have PLI?

Yes. Many clients and businesses now require PLI as a condition of engagement - particularly in healthcare, legal services, and technology consulting. Even where the state doesn't mandate it, it's often effectively required to win contracts and bids.

How can I make sure my PLI coverage will actually respond if a claim is made?

This is the right question to ask. Policy wording, exclusions, and the financial strength of your insurer all matter. A dedicated Risk Advisor will review your coverage in detail - not just the premium - to make sure the policy is structured correctly for your profession and exposure.

Why work with an independent broker rather than going direct?

An independent broker like Thumann Agency isn't tied to any single insurer. That means we can place your risk across 80+ carriers and find the policy that genuinely fits your exposure - not just the one that's easiest to sell. You also get a dedicated advisor who stays with you, rather than a call centre that changes every time you ring.

Speak with a Thumann Risk Advisor Today

If you're a Dallas professional looking for PLI coverage that's built around your actual exposure - not just a number pulled from a comparison site - Thumann Agency is ready to help. Our Risk Advisors take the time to understand your profession, your clients, and your risk before recommending any placement.

From real estate and law to medicine, accountancy, and technology consulting, we've been placing professional liability coverage for Dallas businesses for 30 years. We know the market, we know the risks, and we know how to make sure your coverage holds up.

Talk to one of our helpful agents today, 972.991.9100

Published: 23rd February, 2026.

Author: Lauren Thumann Director of Marketing.

The dollar amounts in this blog are published benchmarks from insurers/brokers and reflect their customer data and assumptions - not a guaranteed “Dallas rate” for every business. Your exact premium can be higher or lower depending on your profession, limits, deductible, revenue, contracts, and claims history.