Running a restaurant in Dallas means managing a constant stream of risk - from a guest slipping on a wet floor during a Friday dinner rush to a hailstorm shutting down your outdoor patio for a week. Thumann Insurance Agency has helped Dallas restaurant owners navigate these exposures since 1996, comparing coverage across 80+ carriers to find the best fit for each operation.

This guide covers what Texas law requires, which policies actually matter for your specific setup, what you'll realistically pay, and how to file a claim correctly if something goes wrong. Whether you run a fine dining room in Uptown, a fast-casual concept off I-35, a food truck at Klyde Warren Park, or a bar in Deep Ellum, the information below is tailored to your situation.

What Does Restaurant Insurance Cover?

Restaurant insurance is a bundle of policies addressing the specific risks food service businesses face. A complete program typically includes:

- General liability - customer injuries, property damage, and foodborne illness claims

- Commercial property - your building, kitchen equipment, inventory, and signage

- Liquor liability - required in Texas for any establishment serving alcohol

- Workers' compensation - employee injuries on the job (optional in TX, strongly recommended)

- Business interruption - lost income and ongoing expenses during covered closures

- Commercial auto - required for any business-owned delivery or catering vehicle

Additional policies - cyber liability, EPLI, equipment breakdown, food spoilage - are layered on based on your specific operation. Every section below explains when each applies and what it costs.

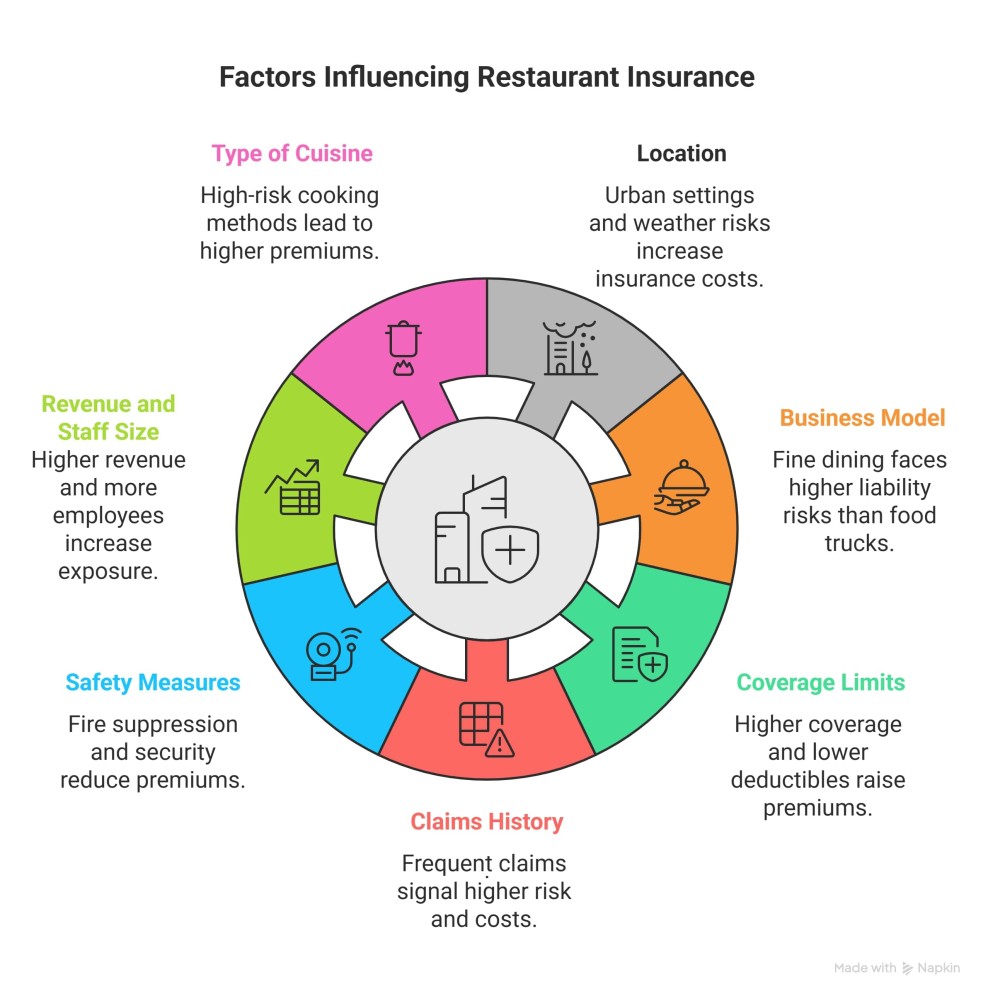

Texas Restaurant Insurance Requirements

Texas does not mandate every policy at the state level, but legal, licensing, and contractual requirements make several coverages effectively non-negotiable for Dallas restaurant owners.

Liquor Liability - Required for Alcohol Service

Any restaurant or bar holding a TABC license must carry liquor liability insurance. Under Texas Dram Shop law, your business can be held financially liable if an overserved guest causes an accident or injury after leaving your establishment. Proof of coverage is required to obtain and maintain your alcohol license. Review requirements at the Texas Alcoholic Beverage Commission.

Commercial Auto - Required for Business-Owned Vehicles

Texas law requires commercial auto insurance on every vehicle your business owns. If your restaurant uses a company van for deliveries or a catering truck for off-site events, this policy is legally mandatory. Texas minimum limits are $30,000 per person / $60,000 per accident / $25,000 property damage - though most carriers and contracts require higher.

HNOA note: If drivers use personal or rented vehicles for restaurant business, you need Hired and Non-Owned Auto (HNOA) coverage separately. Personal auto policies exclude business use and will deny claims that occur during delivery or catering runs.

General Liability & Property - Required by Lease and Permits

Texas state law does not mandate these, but nearly every commercial lease in Dallas requires a minimum of $1M per occurrence general liability as a condition of signing. City of Dallas permits for outdoor dining, alcohol service, and special events also require proof of coverage. SBA loans and most commercial lenders require property insurance tied to the loan value.

Workers' Compensation - Optional in Texas, Strongly Recommended

Texas is the only state that does not require workers' comp. If you opt out, you must file a notice with the Texas Department of Insurance and notify your employees - and you remain personally liable for all workplace injury costs. Given that the restaurant industry logs 3.6 injuries per 100 full-time workers annually, with cuts, burns, and slips dominating claims, most Dallas operators carry it. Workers' comp also includes employer's liability, which shields you from lawsuits if an injured employee claims your negligence caused the harm.

Coverage Types: What You Actually Need and Why

General Liability Insurance

The foundation of any restaurant insurance program. General liability covers third-party bodily injury - a customer slips on a wet floor, trips over an uneven threshold, or burns themselves on a hot dish. It covers property damage to customer belongings and includes product liability, which is the coverage that applies when a guest claims your food made them sick.

Slip-and-fall claims account for roughly 35% of general liability claims in restaurants. Standard limits are $1M per occurrence / $2M aggregate. Your landlord will likely require you to add them as an additional insured before you get keys to the space.

Allergy and Foodborne Illness Liability

Foodborne illness and allergic reaction claims fall under the product liability extension of your general liability policy - they are not a separate purchase. That said, if your menu includes high-risk allergens like shellfish, peanuts, or gluten, confirm your policy explicitly covers product liability and ask about per-claim sublimits. A severe anaphylactic reaction from mislabeled ingredients can generate significant legal exposure quickly.

Business Owner Policy (BOP)

A Business Owner Policy bundles general liability and commercial property into one policy at a lower combined cost than purchasing them separately. Most BOPs for restaurants also include business interruption coverage, which pays lost income and ongoing expenses - rent, payroll, utilities - if a covered event forces you to close temporarily. The average BOP for a Dallas restaurant runs about $251 per month and is the most common starting point for operators in this market.

Liquor Liability Insurance

Mandatory for any TABC-licensed establishment and sold as a standalone policy, because general liability explicitly excludes alcohol-related claims. Liquor liability covers legal fees, settlements, and medical costs from incidents involving overservice - a guest who causes a car accident after leaving your bar, a fight that breaks out after last call, or a minor who was served by a staff member who failed to check ID. In Dallas's nightlife districts, this is one of the highest-exposure coverages on your program.

Workers' Compensation Insurance

Workers' comp covers medical treatment, rehabilitation, and partial wage replacement for employees injured on the job. Kitchen injuries - knife cuts, grease burns, slips on wet floors - are among the most frequent claims in any industry. Coverage also includes employer's liability protection, which defends you if an injured employee files a civil lawsuit claiming your negligence caused the incident.

Commercial Auto Insurance

Commercial auto is legally required for every business-owned vehicle. Dallas traffic on I-35, I-75, and the Tollway creates genuine accident exposure for any restaurant with a delivery van or catering truck. Coverage includes liability for accidents your driver causes, physical damage to your vehicle, and medical payments. Add HNOA coverage if any of your drivers also use personal vehicles for restaurant runs.

Cyber Liability Insurance

Every restaurant that processes credit cards, runs online orders, or stores customer data is a target. A data breach affecting your POS system can trigger customer notification requirements, credit monitoring costs, legal fees, and regulatory fines under Texas law - none of which are covered under a standard business policy. Cyber liability also covers ransomware attacks, which have shut down restaurant point-of-sale systems during peak service hours.

Employment Practices Liability Insurance (EPLI)

The restaurant industry has some of the highest employee turnover rates of any sector, and with turnover comes exposure to wrongful termination, discrimination, harassment, and wage claims. EPLI covers legal defense costs, settlements, and judgments for claims filed by current, former, or prospective employees. Recommended for any Dallas restaurant with five or more employees.

Commercial Umbrella Insurance

A commercial umbrella policy extends your liability limits above the underlying GL or auto policy - typically adding $1M–$5M of additional coverage. If a major lawsuit exceeds your GL limit, the umbrella fills the gap. Essential for fine dining establishments, bars, nightclubs, and any restaurant in high-foot-traffic Dallas corridors.

Equipment Breakdown Insurance

Standard commercial property policies cover fire damage and storm damage but exclude mechanical failure. Equipment breakdown coverage fills that gap - paying for repair or replacement when your walk-in refrigerator motor fails overnight, your commercial oven trips an electrical surge, or your HVAC system goes down during a Dallas August. In a restaurant where downtime costs both revenue and spoiled inventory, this coverage pays for itself quickly.

Food Spoilage Coverage

Added as an endorsement to your BOP or commercial property policy - not sold as a standalone. It covers the cost of replacing perishable inventory lost due to power outages, equipment failure, or refrigeration breakdown. Not included in a standard property policy and must be specifically requested. Any restaurant carrying significant fresh inventory should have this endorsement in place before summer storm season.

How Much Does Restaurant Insurance Cost in Dallas?

Costs depend on your restaurant type, annual revenue, number of employees, whether you serve alcohol, your claims history, and your location. Dallas operators typically pay 10–20% more than statewide averages because of urban density, higher litigation rates, and North Texas hail exposure. The figures below reflect median policy data from actual restaurant purchases - not artificially low minimums.

Cost by Coverage Type

- General Liability: $1,200–$6,000 per year, averaging around $141 per month. Required by most leases at $1M/$2M standard limits.

- Business Owner Policy (BOP): $2,400–$6,300 per year, averaging around $251 per month. Bundles GL and property - the best value for most restaurants.

- Workers' Compensation: $600–$10,000 per year, averaging around $113 per month. Optional in Texas but strongly recommended.

- Liquor Liability: $400–$3,000 per year, averaging around $80 per month. Required for any TABC-licensed establishment.

- Commercial Auto: $1,100–$5,000 per year, averaging around $181 per month. Required for business-owned delivery and catering vehicles.

- Cyber Liability: $500–$2,500 per year, averaging around $100 per month. Recommended for any POS or online ordering system.

- EPLI: $800–$3,500 per year, averaging around $135 per month. Recommended for restaurants with five or more employees.

- Equipment Breakdown: $300–$1,500 per year, averaging around $65 per month. Covers oven, refrigerator, and HVAC failure.

- Commercial Umbrella: $500–$2,000 per year, averaging around $80 per month. Extends GL and auto limits - essential for bars and nightclubs.

Cost by Restaurant Type

-

Food truck: $2,000–$4,500 per year. Core coverages: commercial auto, general liability, equipment property.

- Café or coffee shop: $2,500–$5,500 per year. Core coverages: BOP with patio weather endorsement, workers' comp.

- Fast-casual restaurant (no alcohol): $3,500–$7,000 per year. Core coverages: BOP, workers' comp.

- Full-service restaurant with alcohol: $6,000–$14,000 per year. Core coverages: BOP, liquor liability, workers' comp, EPLI.

- Bar or nightclub: $8,000–$20,000 per year. Core coverages: high-limit liquor liability, general liability, EPLI, commercial umbrella.

- Multi-location restaurant group: Negotiated under a master commercial policy. Typically 15–25% lower per-location cost than insuring each location separately.

Ways to reduce your premium without cutting coverage:

Bundle policies into a BOP rather than buying general liability and property separately

- Install a commercial fire suppression system in the kitchen - required by most Dallas leases and eligible for property premium discounts

- Complete TABC-certified server training for bar staff - multiple carriers discount liquor liability premiums for documented certified programs

- Maintain a clean claims history - even one prior claim can raise premiums 15–25% at renewal

- Install monitored security cameras and alarm systems - eligible for commercial property and crime coverage discounts

Increase your deductible if you have sufficient cash reserves to absorb smaller losses out of pocket

For a complete cost breakdown by restaurant type and coverage tier, read: Average Restaurant Insurance Costs in Texas

Restaurant Insurance by Business Type

Fine Dining Restaurants

High-value interiors, custom kitchen equipment, extensive wine programs, and high customer expectations create elevated liability exposure. Core needs for fine dining: high-limit general liability at $2M aggregate or above, commercial property covering custom ranges, wine cellars, and artwork, liquor liability for wine and cocktail service, and EPLI for formal front-of-house staff structures. Fine dining establishments in Dallas neighborhoods like Highland Park, Knox-Henderson, and Uptown should also carry commercial umbrella coverage above their GL limits.

Fast-Casual and Fast Food Restaurants

High customer volume, drive-thru operations, and delivery fleets create distinct exposures at lower overall premium levels. A BOP is the standard starting point. Add commercial auto for every company-owned delivery vehicle, HNOA if drivers use personal cars, and workers' comp for kitchen and counter staff. For Dallas taco chains or QSR operators with outdoor signage, add a hail endorsement to your property coverage.

Bars and Nightclubs

Liquor liability is the primary and most costly exposure. High-volume alcohol service, late hours, and crowded environments create significant dram shop risk. A commercial umbrella policy above GL limits is standard practice for any Dallas nightclub. EPLI is critical given staff turnover and the frequency of employment claims in late-night hospitality environments.

Food Trucks

Commercial auto is the base policy - the vehicle is both your business and your primary asset. Layer general liability for customer interactions at events and markets, commercial property for cooking equipment and inventory, and event-specific endorsements for Dallas festivals like the State Fair of Texas or Taste of Dallas. These events require vendors to carry minimum coverage and typically name the organizer as additional insured on the certificate. Same-day COI issuance is available for last-minute vendor confirmation requirements.

Cafés and Coffee Shops

Simpler risk profile than full-service restaurants, but Dallas cafés with outdoor patios need a weather endorsement on their property coverage. Espresso equipment is expensive and frequently damaged by power surges - equipment breakdown coverage is worth adding. Business interruption matters when a single power outage can ruin a week's supply of specialty inventory before you open for the day.

Pop-Up and Temporary Restaurants

Short-term general liability can be purchased for single events or seasonal operations. Dallas festival organizers and event venues typically require vendors to carry a $1M GL minimum and name the venue as additional insured. Certificates of Insurance can be issued same-day for last-minute booth confirmations.

Multi-Location Restaurant Groups

Restaurant groups operating multiple Dallas locations should consolidate coverage under a master commercial policy rather than insuring each location separately. This approach typically reduces per-location premiums by 15–25%, streamlines all claims under a single carrier relationship, and ensures consistent coverage limits across your entire operation. An independent agent working across 80+ carriers can negotiate master policy terms that a direct insurer cannot match.

Dallas Restaurant Insurance Checklist

Use this before signing a lease, applying for a permit, or opening for business:

- General liability: Minimum $1M/$2M limits. Landlord named as additional insured on lease.

- Liquor liability: Required if serving alcohol. Proof submitted to TABC before license activation.

- Commercial property: Covers building, equipment, and inventory. Hail endorsement added for Dallas.

- Business interruption: Included in BOP or added as endorsement. Minimum 12 months of income coverage.

- Workers' compensation: Recommended for all restaurants with employees. TDI opt-out notification filed if waived.

- Commercial auto: Required for any business-owned vehicle. HNOA added if drivers use personal vehicles.

- Food spoilage endorsement: Added to BOP. Critical for any restaurant with large perishable inventory.

- Cyber liability: Recommended for any POS, online ordering, or customer data system.

- EPLI: Recommended for restaurants with five or more employees.

- Certificate of Insurance (COI): Same-day issuance available. Required for lease signings, permit applications, and vendor contracts.

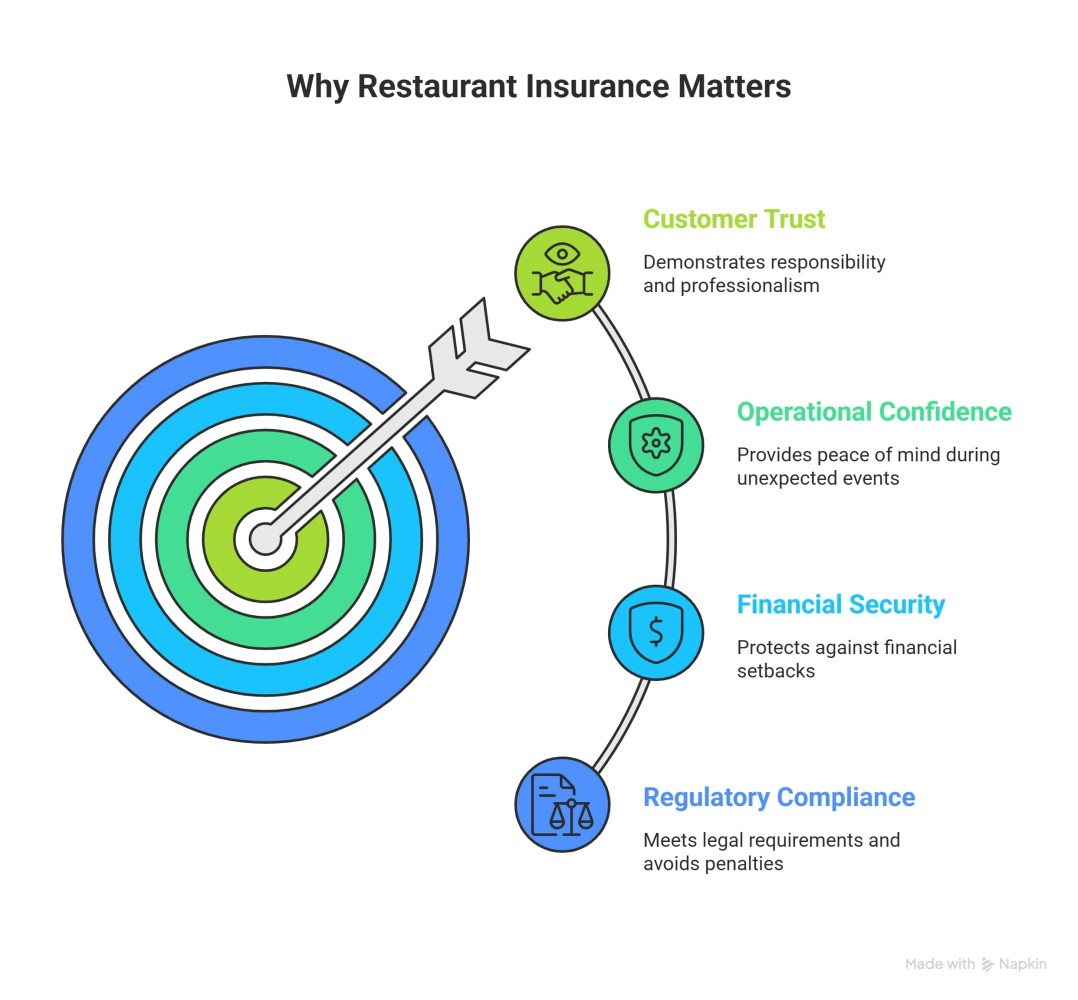

Risk Management for Dallas Restaurants

Insurance pays for what goes wrong. Risk management reduces how often things go wrong - and directly affects what you pay at renewal.

Most Common Restaurant Claims in Texas

- Customer slip-and-fall - Wet floors, unmarked steps, and uneven surfaces account for roughly 35% of GL claims. The single most preventable claim type.

- Kitchen fires - More than 7,000 restaurant fires occur annually across the U.S. Grease buildup in hood systems is the leading cause in Texas commercial kitchens.

- Foodborne illness - A single supplier contamination event or temperature control failure can produce multiple simultaneous claimants, each with independent legal standing.

- Employee injuries - Cuts and burns dominate workers' comp claims. The restaurant industry logs 3.6 injuries per 100 full-time employees annually.

- Alcohol-related incidents - Overservice is the most litigated exposure in Texas hospitality. Dram shop liability claims can exceed standard GL limits, which is why umbrella coverage matters.

- Weather-related property damage - Dallas hail seasons from March through June produce the highest restaurant property claim frequency in Texas. Outdoor signage, patio furniture, and HVAC units are the most frequently damaged assets.

Prevention Strategies That Lower Premiums

- Install commercial fire suppression in the kitchen - required by Dallas fire code and eligible for property premium discounts from most carriers

- Use non-slip mats and post Wet Floor signage consistently; document floor inspection logs to support your defense in any slip-and-fall claim

- Require TABC-certified server training for all bar and service staff - multiple carriers discount liquor liability premiums for documented certified programs

- Implement encrypted payment processing on a network separate from back-office systems to reduce cyber breach exposure

- Conduct quarterly equipment maintenance inspections and keep dated service records - these records accelerate equipment breakdown and property claims

- Install monitored security cameras throughout the dining room, bar, and kitchen - eligible for commercial property and crime coverage discounts

For a detailed prevention framework, read: Risk Management Strategies to Lower Restaurant Insurance Premiums.

Dallas-Specific Weather Risks

Dallas averages five to eight significant hail events per year, with the most active window running March through June. Tornado watches are issued across North Texas multiple times annually. Flash flooding during spring storm systems has closed restaurants in Deep Ellum, Lower Greenville, and the Design District.

Add hail and windstorm endorsements to your commercial property policy - standard Dallas policies frequently exclude these perils in high-risk Texas markets

Add flood coverage if your location falls in or near a FEMA-designated flood zone

Secure outdoor patio furniture and signage before forecast storm events - damage to unsecured property is often outside covered perils

Build a documented business continuity plan identifying temporary kitchen partners, customer communication protocols, and how long your business interruption coverage can sustain operations

How to File a Restaurant Insurance Claim in Texas

Texas regulates claim handling timelines by statute. Missing a reporting deadline is the most common reason legitimate claims get reduced or denied.

- Document immediately: Photograph all damage before anything is moved, cleaned, or repaired. Collect witness names and contact information. Preserve receipts, invoices, and health inspection records for any foodborne illness claim.

- Report within 15 days: Texas Insurance Code requires insurers to acknowledge claims within 15 days of notification. File as soon as possible - ideally within 72 hours even if your documentation is incomplete. Late reporting is the single most common cause of claim delays and denials.

- Submit complete documentation: Provide the incident report, contractor repair estimates, daily revenue records supporting any business interruption claim, and any health department correspondence for food-related claims.

- Cooperate with the adjuster: Allow property inspection before repairs begin. Respond to information requests promptly. Adjusters have 15 business days to approve or deny after receiving your documentation.

- Receive payment: Approved claims must be paid within 5 business days of approval under Texas Insurance Code §542.058.

Common mistakes that reduce or delay restaurant claims:

-

Disposing of spoiled food or damaged equipment before the adjuster inspects it

- Beginning repairs before getting a formal contractor bid for the adjuster to review

- Not tracking daily revenue with sales records to support a business interruption claim

- Filing late - even 20 days after an incident can create a coverage dispute

Why Dallas Restaurant Owners Work With Thumann Agency

As an independent agency with access to 80+ carriers, Thumann Agency shops the full market on your behalf - including specialty restaurant programs not available through direct writers. That means your premium is subject to real competition, not a single company's rate table.

- Same-day COIs for lease signings, permit applications, and vendor contracts

- Coverage comparisons across 80+ carriers, including specialty programs for bars, nightclubs, and food trucks

- Local agents who understand TABC requirements, Dallas permit standards, Deep Ellum liquor liability exposure, and North Texas hail risk

- Annual policy reviews as your operation evolves - adding a location, launching delivery, adding alcohol service, or expanding catering

See what Dallas restaurant owners say on our Google reviews, or call (972) 991-9100 to compare quotes today.

Frequently Asked Questions

What insurance does a restaurant need to open in Dallas?

At minimum: general liability (required by your commercial lease), commercial property (required by your landlord or lender), and liquor liability if serving alcohol. A Certificate of Insurance naming the City of Dallas or your landlord as additional insured is typically required before permits are issued. Workers' comp and commercial auto should be added based on your staff size and whether you operate delivery vehicles.

Is restaurant insurance mandatory in Texas?

Liquor liability is mandatory for any TABC-licensed establishment. Commercial auto is required for business-owned vehicles. General liability and property are required by most commercial leases and permit authorities. Workers' compensation is optional in Texas but strongly recommended for any restaurant with employees.

How much does restaurant insurance cost in Dallas, TX?

A food truck typically pays $2,000–$4,500 per year. A fast-casual restaurant without alcohol runs $3,500–$7,000. A full-service restaurant with alcohol service ranges from $6,000–$14,000. Bars and nightclubs often pay $8,000–$20,000 or more. Dallas premiums run 10–20% higher than statewide averages due to urban density and hail exposure.

What is a BOP and do Dallas restaurants need one?

A Business Owner Policy bundles general liability and commercial property insurance at a lower combined cost than buying them separately. It typically includes business interruption coverage as well. The average BOP for a Dallas restaurant costs around $251 per month and is the most cost-effective starting point for most operations.

Does restaurant insurance cover food spoilage?

Standard policies do not. Food spoilage is added as an endorsement to your BOP or commercial property policy. It covers inventory lost due to power outages, equipment failure, or refrigeration breakdown. Given Dallas's summer heat and frequent storm-related power outages, this endorsement is worth adding if you carry significant perishable inventory.

What is liquor liability and is it required in Texas?

Liquor liability covers legal fees, medical costs, and settlements arising from alcohol-related incidents including overservice, dram shop claims, and alcohol-related fights on your premises. It is required for any Texas establishment holding a TABC license and is sold as a separate policy because general liability explicitly excludes alcohol-related claims.

Can I get same-day restaurant insurance in Dallas?

Yes. Certificates of Insurance can typically be issued the same day. If you need a COI for a lease signing, a City of Dallas permit, or a vendor contract naming your landlord or organizer as additional insured, call (972) 991-9100 and we can typically process it within hours.

Does restaurant insurance cover cyberattacks or data breaches?

Standard restaurant policies do not. Cyber liability is a separate policy covering breach response, customer notification, credit monitoring, legal fees, and business losses from ransomware or system downtime. Any restaurant running a POS system, online ordering, or a customer loyalty program should have cyber liability coverage in place.

What is EPLI and do Dallas restaurants need it?

Employment Practices Liability Insurance covers wrongful termination, discrimination, harassment, and wage dispute claims from current, former, or prospective employees. Given the restaurant industry's high turnover rates and complex scheduling, EPLI is recommended for any Dallas restaurant with five or more employees. A single employment claim without coverage can cost $50,000–$150,000 in legal fees and settlement.

What insurance do I need for outdoor dining in Dallas?

General liability covering customer injuries in the outdoor space, commercial property with a hail and windstorm endorsement for patio furniture and structures, and in some cases a specific City of Dallas sidewalk café permit endorsement. Standard property policies frequently exclude hail and wind damage in Texas markets - confirm your endorsements explicitly cover these perils.

What type of insurance does a food truck need in Dallas?

Commercial auto insurance for the vehicle itself (legally required), general liability for customer interactions at events and markets, commercial property for cooking equipment and inventory, and event-specific endorsements when operating at festivals or city venues that require vendor coverage. Same-day COIs available for last-minute confirmations.

What happens if I don't have restaurant insurance?

You bear 100% of all claim costs personally - including legal defense, settlements, property repairs, and lost income during closure. You also risk losing your TABC license, your commercial lease, and any business financing or SBA loan secured against your operation.

Get a Restaurant Insurance Quote in Dallas, TX

Restaurant coverage is not a one-size-fits-all product. A food truck has different needs than a fine dining room, and a Dallas bar faces different exposure than a suburban fast-casual location. Thumann Insurance Agency has been placing restaurant insurance in Dallas since 1996, comparing options across 80+ carriers to match each operation with the right program at the right price.

Call (972) 991-9100 or submit a restaurant insurance quote request online. Same-day COIs available for lease signings and permit applications.

Last Updated: 25 February 2026

Author: Lauren Thumann Director of Marketing.

Disclaimer: This page is for educational purposes only. Coverage details vary by provider. Contact us for a personalized quote.