Running a business in Dallas, Texas, involves managing numerous responsibilities, including protecting vehicles used for work. Whether your company operates delivery vans, construction trucks, or corporate cars, commercial auto insurance in Dallas is essential for safeguarding your operations. This type of insurance is tailored for vehicles used in business activities, covering risks that personal auto policies do not, such as liability for employee-caused accidents or damage to company-owned vehicles.

This guide offers a comprehensive, unbiased resource to help you understand business vehicle coverage. It explains what it is, its importance, available coverage types, costs, and strategies for managing risks, with a focus on Dallas’s unique environment. Designed for business owners ranging from beginners to those refining existing policies, this content provides detailed insights into the science, history, and practical aspects of commercial auto insurance. By the end, you’ll be equipped to make informed decisions to protect your business on the road.

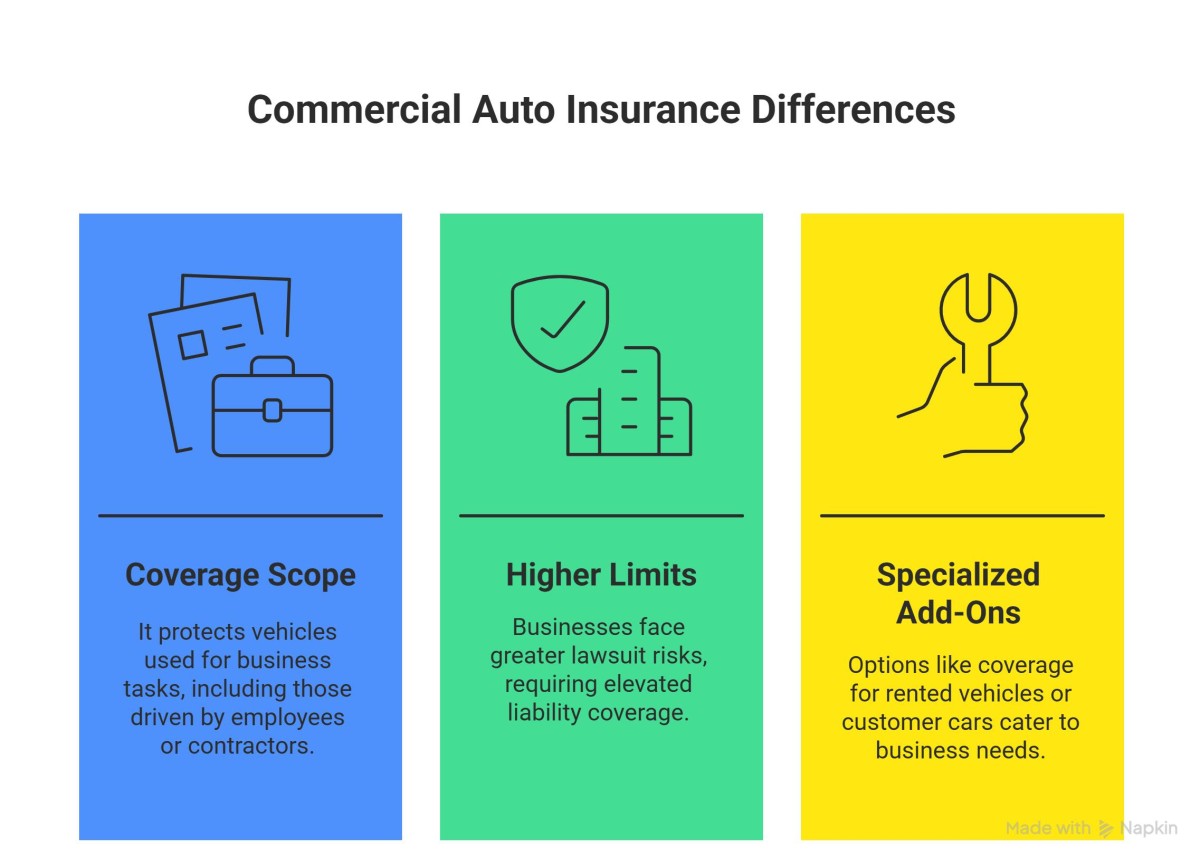

What is Commercial Auto Insurance?

Commercial auto insurance is a specialized policy for vehicles used in business operations. This includes company cars for client meetings, delivery vans for transporting goods, or trucks for construction projects. Unlike personal auto insurance, which covers individual drivers for non-work purposes, this insurance addresses risks unique to businesses, such as liability for accidents caused by employees or damage to costly work vehicles.

Key differences from personal auto insurance include:

-

Coverage Scope: It protects vehicles used for business tasks, including those driven by employees or contractors.

-

Higher Limits: Businesses face greater lawsuit risks, requiring elevated liability coverage.

-

Specialized Add-Ons: Options like coverage for rented vehicles or customer cars cater to business needs.

For example, a Dallas-based plumbing company using vans to transport tools needs this insurance to cover accidents or equipment damage, which a personal policy wouldn’t address. The history of commercial auto insurance traces back to the early 20th century, when businesses began using vehicles for commerce, prompting insurers to develop policies for these new risks. Today, it’s a cornerstone of business risk management.

Importance of Commercial Auto Insurance

This insurance is a legal requirement in Texas for businesses operating vehicles, but its value goes beyond compliance. It ensures businesses can cover damages or injuries caused by their vehicles, protecting both the company and the public. Financially, it shields against the high costs of accidents, repairs, or lawsuits, which could destabilize a small business.

In Dallas, where traffic congestion, urban risks, and severe weather are prevalent, business vehicle coverage provides stability. It allows owners to focus on operations without worrying about vehicle-related incidents. For instance, a retail business making local deliveries benefits from knowing an accident won’t halt its operations. A 2024 study by the Insurance Information Institute found that businesses with comprehensive insurance recover 30% faster from accidents than those without, highlighting its role in continuity.

Types of Commercial Auto Insurance

Understanding coverage types is crucial for tailoring a policy to your business. Below are the main options and their applications.

Liability Coverage

Liability coverage is the core of commercial auto insurance, covering bodily injury and property damage your vehicle causes to others. For example, if an employee causes a crash in Dallas, this coverage pays for the other party’s medical bills or vehicle repairs, up to the policy’s limits.

Texas requires minimum limits of 30/60/25:

-

$30,000 per person for bodily injury

-

$60,000 per accident for bodily injury

-

$25,000 for property damage

These minimums may be insufficient for businesses with significant assets, as urban claims often exceed them. A 2023 report by the Texas Department of Insurance noted that liability claims in cities like Dallas average $45,000, prompting many businesses to choose higher limits for better protection.

Physical Damage Coverage

Physical damage coverage protects your vehicles from damage, regardless of fault. It includes:

-

Collision: Covers repairs after accidents with vehicles or objects, like hitting a pole during a delivery.

-

Comprehensive: Covers non-collision incidents, such as theft, vandalism, or hail damage, common in Dallas.

This coverage is vital for businesses with valuable vehicles, like a construction firm with specialized trucks. Comprehensive coverage is particularly relevant in Texas, where a 2024 National Weather Service report recorded 15 severe hail events in Dallas in 2023, causing millions in vehicle damage.

Uninsured/Underinsured Motorist Coverage

Uninsured motorist coverage protects your business if an at-fault driver lacks adequate insurance. In Dallas, heavy traffic increases accident risks, and this coverage ensures your business isn’t left paying for repairs or medical costs. For example, if an uninsured driver hits your company car, this coverage helps cover damages. The Texas Department of Insurance estimates 8% of Texas drivers are uninsured, making this coverage essential in urban areas.

Medical Payments Coverage

Medical payments coverage pays for medical expenses for your driver and passengers, regardless of fault. This is valuable for businesses with employees who drive company vehicles, like a logistics company. It covers hospital visits, surgeries, or funeral costs in severe cases, offering quick financial relief. Unlike liability coverage, which focuses on third parties, this prioritizes your team’s health.

Specialized Coverages

Businesses with unique needs may require additional coverages:

-

Hired auto coverage protects vehicles not owned by your business but used for work, like a rented van for a project.

-

Garagekeepers Legal Liability: For businesses like repair shops that store customer vehicles.

-

Towing and Labor: Covers roadside assistance, such as towing or tire repairs.

-

Cargo Coverage: Protects goods transported in your vehicles, crucial for delivery businesses.

Why Businesses Need Commercial Auto Insurance

Legal Requirements

Texas law mandates commercial auto insurance for vehicles used in business, with minimum liability limits of 30/60/25. This applies to vehicles registered to a business or used for tasks like deliveries or equipment transport. Federal rules may also apply for interstate commerce or industries like trucking. Non-compliance risks fines, license suspension, or legal penalties, making insurance mandatory for Dallas businesses.

Financial Protection

This insurance protects against significant financial losses from:

-

Vehicle repair costs

-

Medical expenses for injuries

-

Legal fees from lawsuits

-

Lost revenue from out-of-service vehicles

For example, a Dallas catering company could face $50,000 in costs if a delivery van is damaged in a crash. A 2024 National Safety Council report estimated commercial vehicle accidents cost businesses $80,000 on average, emphasizing the need for robust coverage.

Operational Continuity

With proper coverage, you can focus on business growth without vehicle-related concerns. In Dallas, where traffic and weather pose challenges, business vehicle coverage ensures continuity. A small business with limited resources benefits from the assurance that an accident won’t derail operations, allowing focus on serving customers.

How to Choose Commercial Auto Insurance

Selecting the right policy requires careful planning. Here’s how to approach it.

Assessing Business Needs

Evaluate your business’s requirements:

-

Vehicle Count and Type: Do you operate one van or a fleet of trucks?

-

Usage: Are vehicles for local deliveries, long-haul transport, or employee commuting?

-

Drivers: How many employees drive, and what are their records?

-

Cargo: Do you transport valuable goods or equipment?

A Dallas construction company may need coverage for heavy trucks, while a retail business requires insurance for delivery vans. Documenting these details helps identify necessary coverage.

Understanding Coverage Options

Match coverage to your risks. A delivery service might prioritize liability and cargo protection, while a landscaping firm needs physical damage coverage for equipment-heavy vehicles. Specialized options like hired auto coverage are relevant if employees use personal cars for work. Reviewing operations with an expert can identify coverage gaps.

Consulting Insurance Experts

An agent familiar with Dallas insurance and Texas regulations can tailor your policy to local risks, like traffic or hailstorms. They explain complex options, recommend limits, and ensure compliance. For example, they might suggest higher liability limits for urban delivery services to cover lawsuit risks.

Comparing Quotes

Obtain quotes from multiple insurers to balance cost and coverage. Compare:

-

Coverage limits and exclusions

-

Deductibles

-

Insurance premiums

-

Insurer reputation

Online tools can streamline comparisons, but verify policies meet Texas requirements. A 2023 Insurance Journal study found businesses comparing at least three quotes saved 15% on average.

Cost of Commercial Auto Insurance

Factors Affecting Premiums

Insurance premiums depend on:

-

Vehicle Count: More vehicles increase costs.

-

Business Type: High-risk industries like construction pay more.

-

Claims History: Past accidents raise rates.

-

Driver Records: Clean records lower costs.

-

Location: Dallas’s traffic and risks elevate premiums.

-

Coverage Limits: Higher limits increase costs.

-

Vehicle Value: Expensive trucks cost more to insure.

A 2024 Progressive Insurance report noted urban areas like Dallas have premiums 12% higher than rural areas due to accident risks. Want to lower your premium? Learn more about what factors affect commercial auto insurance premiums in Texas in our detailed guide.

Average Costs in Texas and Dallas

Insureon reports Texas’s average monthly cost is $218 ($2,610 annually). In Dallas, premiums are higher due to urban risks, with delivery services paying $250-$350 monthly per van and construction firms exceeding $6,000 annually for multiple trucks. Costs vary by industry and coverage. Consult an agent for accurate quotes.

Cost-Saving Strategies

Reduce costs by:

-

Bundling Policies: Combine auto and liability insurance.

-

Safety Programs: Train drivers to reduce accidents.

-

Screening Drivers: Hire those with clean records.

-

Higher Deductibles: Lower premiums with higher out-of-pocket costs.

-

Comparing Quotes: Shop for the best rates.

A 2024 Insurance Journal study found safety programs cut premiums by 18% over three years.

Commercial Auto Insurance Regulations in Texas

State Mandates

Texas regulations require businesses to carry commercial auto insurance with 30/60/25 liability limits. Policies must comply with the Texas Department of Insurance (TDI), ensuring coverage for damages or injuries. Proof of insurance is needed for vehicle registration and some contracts.

Dallas-Specific Factors

Dallas’s urban setting increases risks:

-

Traffic: Higher accident rates raise premiums.

-

Theft: Urban areas require comprehensive coverage.

-

Weather: Hail and flooding lead to frequent claims.

A 2024 TDI report noted Dallas had 20% more vehicle claims than rural Texas due to these factors.

Required Filings

Businesses like trucking firms may need to file proof of insurance, such as a BMC-91 form for interstate commerce. Ensure compliance to avoid penalties.

Finding Commercial Auto Insurance in Dallas, Texas

Local Agents and Brokers

Local insurers in Dallas offer:

-

Regional Expertise: Knowledge of traffic and weather risks.

-

Tailored Policies: Coverage for your business’s needs.

-

Multiple Quotes: Access to various insurers.

Agencies like Thumann Agency provide personalized guidance. Contact Thumann Agency at (972) 991-9100 or visit thumannagency.com for assistance.

Online Comparison Tools

Online platforms like Insureon allow quick quote comparisons. Ensure policies meet Texas regulations and address Dallas risks, like hail damage.

Advantages of Dallas-Based Providers

Dallas insurance providers understand local challenges, recommending coverage for urban accidents or weather damage. They ensure compliance and practicality, such as higher limits for delivery services.

The Claims Process for Commercial Auto Insurance

Filing a Claim

For an incident:

-

Document: Take photos, get police reports, and collect witness statements.

-

Notify Insurer: Report within 15 days per TDI rules.

-

Submit Details: Provide accurate documentation.

Prompt reporting ensures a smooth claims process.

Navigating the Claims Process

TDI mandates insurers:

-

Respond within 15 days

-

Decide within 15 business days after documentation

Adjusters assess damage and determine payouts. Complex claims may take longer, but communication speeds resolution.

Avoiding Common Errors

Ensure success by:

-

Reporting promptly

-

Providing complete documentation

-

Avoiding misrepresentations

A 2024 TDI report cited incomplete documentation as the top cause of delayed claims. For a detailed step-by-step breakdown, visit our Commercial Auto Insurance Claim Process in Dallas guide.

Risk Management for Commercial Auto

Implementing Safety Measures

Safety protocols reduce accidents:

-

Training: Offer defensive driving courses.

-

Maintenance: Inspect vehicles regularly.

-

Telematics: Monitor driving behavior.

A 2023 NHTSA study found telematics cut fleet accidents by 16%.

Preventing Claims

Install:

-

Dash cams for accident evidence

-

Anti-theft systems

-

Backup cameras for urban driving

Review driver records to enforce safety.

Managing Weather Risks in Dallas

Dallas’s hail, tornadoes, and floods require:

-

Emergency plans

-

Covered parking

-

Comprehensive coverage

A 2024 National Weather Service report noted 14 severe hail events in Dallas in 2023.

Commercial Auto Insurance for Specific Industries

Transportation and Logistics

Fleet insurance for trucking includes:

-

Long-haul truck coverage

-

Cargo protection

-

Driver liability

Higher limits are needed for federal compliance.

Delivery Services

Delivery businesses need:

-

Van coverage

-

Cargo protection

-

Hired auto for employee vehicles

Comprehensive coverage addresses theft risks.

Construction

Construction firms require:

-

Truck and equipment coverage

-

Tool transport protection

-

On-site liability

Physical damage coverage is critical for costly equipment.

Ridesharing and Car-Sharing

Ridesharing needs:

-

Passenger liability

-

App-on period coverage

-

Vehicle wear protection

Policies blend commercial and personal coverage.

Other Dallas Industries

-

Oil and Gas: Tanker coverage.

-

Manufacturing: Delivery insurance.

-

Retail: Van coverage for deliveries.

Frequently Asked Questions (FAQs)

Is commercial auto insurance mandatory in Texas?

Yes, businesses operating vehicles need it with 30/60/25 limits.

What does commercial auto insurance cover?

It includes liability coverage, physical damage, medical payments, and specialized options like hired auto.

How much is commercial auto insurance in Dallas?

Texas averages $218/month; Dallas may be 12% higher due to risks (Insureon).

Can I bundle commercial auto insurance?

Yes, bundling with liability insurance saves money.

How can I reduce insurance premiums?

Train drivers, bundle policies, raise deductibles, and compare quotes.

Does it cover personal vehicles used for work?

Only with hired auto coverage.

What are Texas’s liability limits?

30/60/25 for bodily injury and property damage.

How does Dallas’s environment affect premiums?

Traffic and theft increase Dallas insurance costs.

What to do after an accident?

Document, notify insurer within 15 days, and submit details.

Are discounts available?

Yes, for safe driving or bundling.

How long is the claims process?

Insurers respond in 15 days and decide in 15 business days (TDI).

Can I insure one vehicle?

Yes, policies fit single vehicles or fleets.

What if I lack insurance?

Fines, suspension, and liability risks apply.

Does it cover theft?

Yes, with comprehensive coverage.

How often should I review my policy?

Annually or after business changes.

What’s hired auto vs. non-owned?

Hired covers rented vehicles; non-owned covers employee vehicles.

Can I add roadside assistance?

Yes, towing coverage is available.

Does it cover cargo?

Yes, cargo coverage protects transported goods.

How does Dallas weather affect coverage?

Hail and floods necessitate comprehensive coverage.

Can I customize my policy?

Yes, tailor coverage to your needs.

Final Thoughts

Commercial auto insurance is vital for Dallas businesses, ensuring compliance, financial protection, and continuity. From liability coverage to fleet insurance, policies safeguard vehicles and operations. Dallas’s traffic, theft, and weather risks make tailored coverage essential. Evaluate needs, compare quotes, and implement safety protocols to optimize protection. Regular policy reviews adapt to business or regulatory changes.

For guidance, contact Thumann Agency, serving Dallas and Texas, at (972) 991-9100 or thumannagency.com

Last Updated: 14.07.2025

Author: Lauren Thumann Director of Marketing.

Disclaimer: This page is for educational purposes only. Coverage details vary by provider. Contact us for a personalized quote.